.png)

Global Disruptions Are Reshaping MSME Risk. Can Traditional Lending Models Keep Up?

Get In Touch

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

For years, MSME lending in India has been built around familiar risk indicators—credit scores, banking behaviour, financial statements, collateral coverage, and repayment history. While these factors remain important, recent global events are highlighting a new reality: borrower risk is no longer determined solely by what happens within a business. Increasingly, it is influenced by what happens outside it.

The ongoing geopolitical tensions in West Asia provide a timely example. According to recent industry estimates, India's MSME sector could witness a moderation in revenue growth by nearly 100 basis points during the current fiscal, while profitability is expected to decline by 50–100 basis points. Sectors dependent on energy-intensive production, imported raw materials, and export markets are likely to face the greatest pressure.

For lenders, this raises an important question: can traditional lending models accurately assess risk in an environment where global disruptions can rapidly alter aborrower's cash flow profile?

When External Events Become Credit Events

MSMEs contribute nearly 30% of India's GDP, account for almost 45% of exports, and support over 110 million jobs. Yet many of these businesses operate with limited financial buffers, making them particularly vulnerable to sudden changes in input costs, supply chain disruptions, and export demand fluctuations.

The current West Asia conflict illustrates how quickly external events can influence business performance. Industries dependent on natural gas, crude derivatives, imported chemicals, and export trade routes are already experiencing cost pressures and operational disruptions.

For example, the Morbi ceramic cluster, responsible for over 80% of India's ceramic tile production, relies heavily on gas-based manufacturing and exports a significant portion of its production to international markets. Similarly, textile businesses in Surat, chemical manufacturers in Gujarat, and smaller pharmaceutical firms dependent on imported raw materials are facing increasing uncertainty around costs and margins.

While these businesses may still appear financially healthy based on historical statements and bureau reports, their future repayment capacity could be significantly affected by evolving market conditions.

This creates agrowing challenge for lenders that rely primarily on static underwriting frameworks.

The Limitation of Traditional MSME Risk Assessment

Most MSME Lending decisions continue to be driven by historical data. Credit reports evaluate past repayment behavior. Financial statements provide a backward-looking view of performance. Even conventional scorecards are designed to assess risk based on established patterns.

However, geopolitical disruptions do not follow historical patterns.

A borrower with a strong repayment record today may experience severe stress tomorrow if raw material costs increase by 30%, export demand weakens, or production capacity is reduced due to supply shortages.

In such situations, lenders may find themselves reacting to risk after it has already materialized rather than identifying warning signals in advance.

The challenge is no longer just about evaluating borrower strength. It is about understanding sectoral exposure, geographic concentration, supply chain dependencies, and emerging economic risks that can affect entire borrower segments simultaneously.

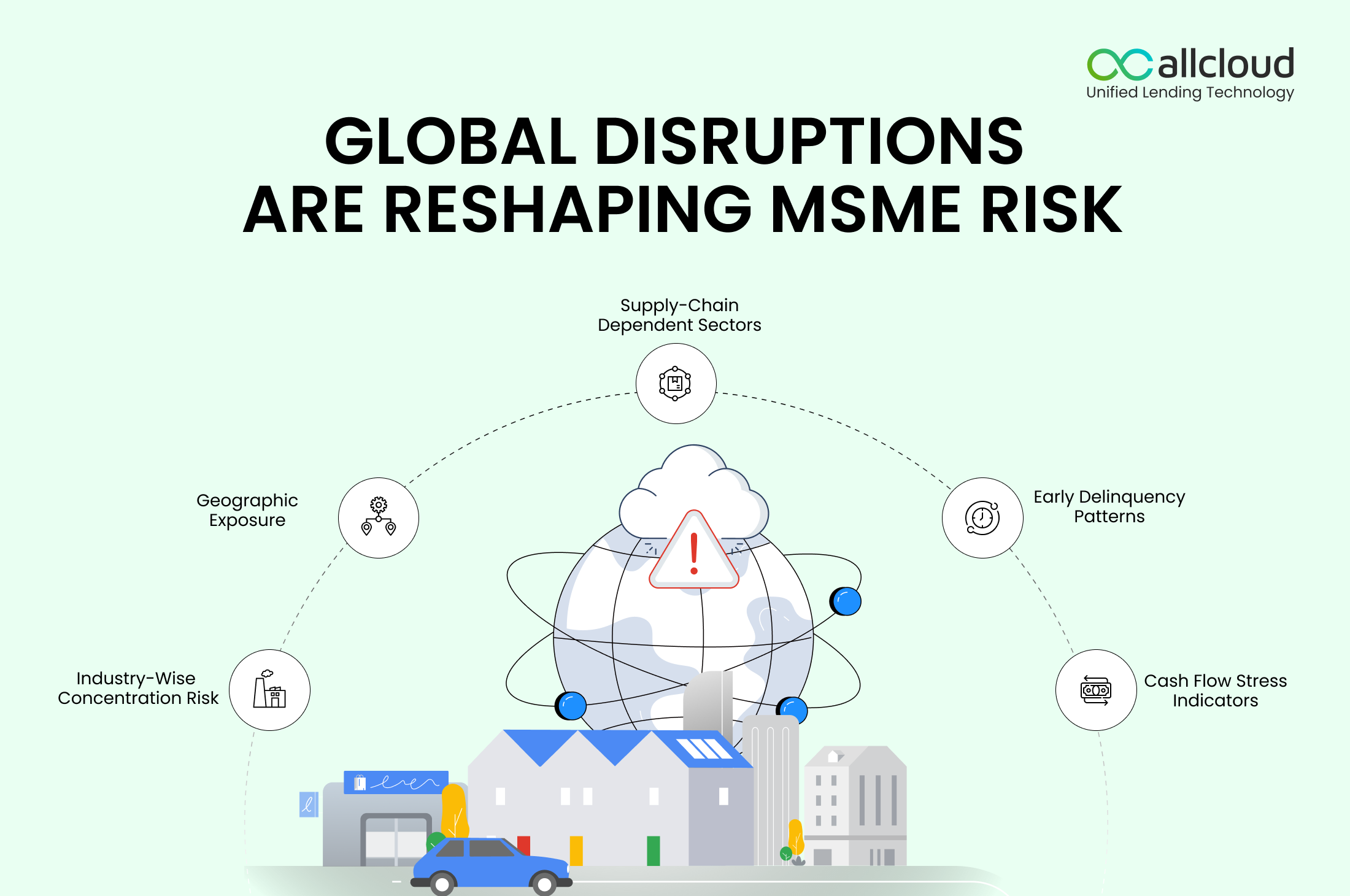

Why Portfolio Visibility Matters More Than Ever?

The impact of global disruptions is rarely uniform across an entire lending portfolio. Certain industries may experience minimal impact, while others face significant perational challenges. Some geographic clusters may remain resilient, while export-oriented regions could experience higher volatility.

For MSME Lenders, this makes portfolio-level intelligence increasingly important. Instead of evaluating borrowers in isolation, lenders need visibility into:

- Industry-wise concentration risk

- Geographic exposure

- Supply-chain dependent sectors

- Early delinquency patterns

- Cash flow stress indicators

- Emerging borrower behavior trends

The ability to identify which borrower segments are becoming vulnerable allows lenders to take proactive measures before repayment performance deteriorates. In an uncertain economic environment, portfolio monitoring becomes as important as underwriting itself.

The Shift from Reactive to Predictive Lending

The Future of MSME lending will likely be defined by how effectively lenders can move from reactive decision-making to predictive risk management. Rather than waiting for missed payments or delinquency triggers, lenders must continuously evaluate portfolio health using operational, behavioral, and market-driven indicators.

For example, lenders may need to monitor:

- Changes in repayment behavior

- Increased utilization of working capital facilities

- Sector-specific stress signals

- Regional economic disruptions

- Borrower engagement patterns

- Collection performance trends

Such insights enable lenders to recalibrate risk strategies, adjust underwriting policies, prioritize collection efforts, and manage exposure before risks translate into losses. This shift requires technology platforms capable of connecting Origination, Servicing, Analytics, and Collections into a unified operational framework.

Building Resilience Through Digital Lending Infrastructure

Periods of economic uncertainty often reveal the strengths and weaknesses of lending operations. Lenders with fragmented systems frequently struggle to gain a consolidated view of portfolio performance, borrower behavior, and risk concentration. Decision-making becomes slower, visibility declines, and operational teams spend more time gathering information than acting on it.

On the other hand, institutions equipped with integrated lending platforms are better positioned to respond quickly to changing market conditions.

A Modern Lending ecosystem enables lenders to:

- Monitor portfolio performance in real time

- Identify vulnerable borrower segments

- Standardize risk assessment processes

- Automate policy-driven lending decisions

- Track collections performance across portfolios

- Improve operational agility during periods of market stress

As Geopolitical and Economic disruptions become more frequent, resilience will increasingly depend on the quality of lending infrastructure rather than the size of the lending portfolio alone.

How AllCloud Helps MSME Lenders Navigate Uncertainty

At AllCloud,we believe that modern MSME lending requires more than digitization. It requires visibility, control, and adaptability. Our Unified Lending Technology platform enables MSME lenders to manage the complete lending lifecycle—from borrower onboarding and credit assessment to Portfolio monitoring, Servicing, and Collections—through a single integrated ecosystem.

With AllCloud, lenders can:

- Digitize MSME Onboarding and Credit Evaluation workflows

- Configure risk-based underwriting policies

- Gain portfolio-level visibility across products, geographies, and borrower segments

- Monitor collection performance and delinquency trends

- Automate operational workflows to improve decision-making speed

- Access analytics that support proactive portfolio management

As lending risks evolve beyond traditional credit parameters, technology must evolve aswell. The ability to identify emerging risks, respond quickly, and maintain portfolio quality will become a critical competitive advantage for MSME Lenders.