.png)

Loan Origination System Evaluation Checklist for Banks and NBFCs: How to Choose the Right Platform in 2026

Get In Touch

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

In today’s lending landscape, choosing the right Loan Origination System is no longer just a technology decision—it is a strategic business move that directly impacts growth, credit quality, compliance, and customer experience.

For banks and NBFCs, the pressure to process loans faster, maintain strict credit policies, and deliver seamless borrower journeys has never been higher. Yet, many lenders continue to operate on fragmented systems, manual workflows,and disconnected tools that slow down operations and introduce risk at scale.

This is where a modern Loan Origination System (LOS) becomes critical. But with dozens of vendors in the market, each promising automation,speed, and intelligence, how do you evaluate and choose the right platform?

More importantly, how do you ensure the system you select doesn’t become another bottleneck in your lending operations?

This blog breaks down a practical, operator-first Loan Origination System evaluation checklist specifically for banks and NBFCs, helping you make a decision that supports long-term scale, control, and profitability.

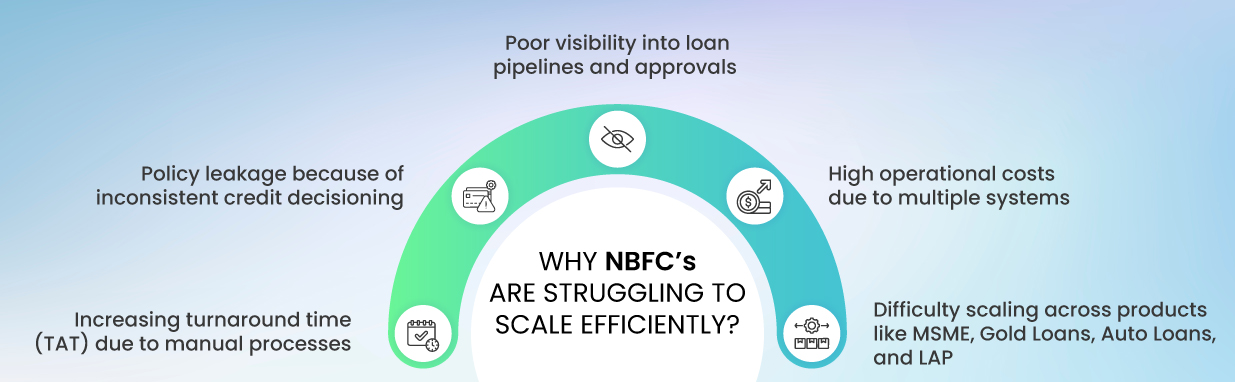

Why Choosing the Right Loan Origination System Matters

Before diving into the checklist, it’s important to understand the stakes. A poorly chosen LOS doesn’t just affect your front-end loan journey—it creates ripple effects across Underwriting, Compliance, Servicing, and Collections.

A well-designed Loan Origination System solves these challenges by bringing structure, automation, and intelligence into the lending process. However, not all systems are built equally—and that’s where a structured evaluation becomes essential.

1. Workflow Flexibility and Configurability

The first and most important factor in evaluating a Loan Origination System is its ability to adapt to your lending workflows. Every lender operates differently— credit policies, approval hierarchies, documentation requirements, and risk frame works vary across institutions and loan products.

A Strong LOS should allow:

- Configurable workflows across loan types

- Multi-level approval structures

- Customizable eligibility checks

- Dynamic rule-based routing

If your system requires constant vendor dependency for workflow changes, it will slow down your business. The right platform should empower your internal teams to configure and manage workflows independently.

2. Rule Engine for Credit Decisioning

Credit decisioning is where most lenders lose control—not because policies are weak, but because execution is inconsistent. A robust rule engine ensures that every application is evaluated based on predefined conditions, without manual interpretation.

Look for:

- Product-specific eligibility rules

- Automated deviation handling

- Configurable approval matrices

- Audit trails for every decision

For NBFCs handling multiple loan products, this becomes critical. A strong rule engine ensures policy consistency, faster approvals, and better auditability.

3. Multi-Product Lending Capability

Most legacy Loan Origination Systems are designed for asingle product or require heavy customization for new loan types. This creates operational silos and increases cost.

The ideal LOS should allow lenders to launch and manage multiple products within a single platform, without rebuilding workflows from scratch.

4. Integration Ecosystem

A Loan Origination System does not operate in isolation. It must integrate seamlessly with third-party systems to enable End-to-End lending operations.

Key integrations include:-

- Credit bureaus

- Account Aggregator frameworks

- Bank statement analysers

- eKYC and verification APIs

- Payment gateways

- Document management systems

The depth and ease of integration determine how efficiently your lending process runs. API-first architecture is no longer optional—it isessential.

5. Turn around Time (TAT) Optimization

Speed is a competitive advantage in lending. Borrowers today expect faster approvals and disbursements, and any delay can lead to drop-offs.

A strong Loan Origination System should:

- Automate data capture and validation

- Reduce manual intervention

- Enable parallel processing of tasks

- Provide real-time application tracking

The goal is not just speed, but controlled speed—ensuring faster approvals without compromising credit quality.

6. Compliance and Audit Readiness

For banks and NBFCs, compliance is non-negotiable. Regulatory requirements continue to evolve, and lenders must ensure that their systems can adapt quickly.

Your LOS should support:

- Complete audit trails

- Role-based access controls

- Data security and encryption

- Regulatory reporting capabilities

- Consent-based data usage

A system that embeds compliance into workflows reduces riskand ensures readiness for audits at any time.

7. User Experience for Internal Teams

While borrower experience is important, internal user experience is often overlooked. Loan officers, credit teams, and operations staff spend hours on the system daily.

A well-designed LOS should:

- Simplify application processing

- Provide intuitive dashboards

- Reduce screen switching

- Enable faster data entry and validation

Better user experience leads to higher productivity and fewer errors.

8. Scalability and Performance

As your lending business grows, your system should scale with you. Many lenders face challenges when their LOS cannot handle increased volumes or new geographies.

Evaluate:

- System performance under high volumes

- Ability to onboard new branches or partners

- Multi-tenant or multi-entity capabilities

- Cloud-native architecture

Scalability is not just about handling more applications—it’s about enabling business expansion without operational disruption.

9. Data Visibility and Analytics

Data-driven decision-making is becoming central to lending. Your Loan Origination System should provide actionable insights, not just process applications.

Look for:

- Real-time dashboards

- Funnel visibility (application to disbursement)

- Approval and rejection analytics

- Performance tracking across branches and products

This helps lenders identify bottlenecks, improve conversion rates, and optimize operations.

10. End-to-End Lending Integration

One of the biggest mistakes lenders make is evaluating LOS in isolation. Origination is just one part of the lending lifecycle. If your LOS does not connect seamlessly with loan management and collections, you will face operational gaps.

A modern approach is to adopt a Unified Lending Technology platform, where LOS, LMS, and collections are tightly integrated.

This ensures:

- Smooth data flow across lifecycle

- Better borrower tracking

- Stronger control over repayments and collections

- Improved customer experience